Huatai Futures: Downstream demand increases cotton bottom uplift

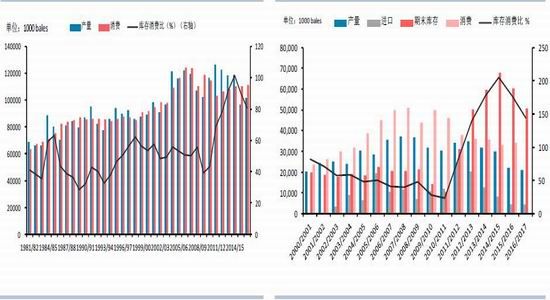

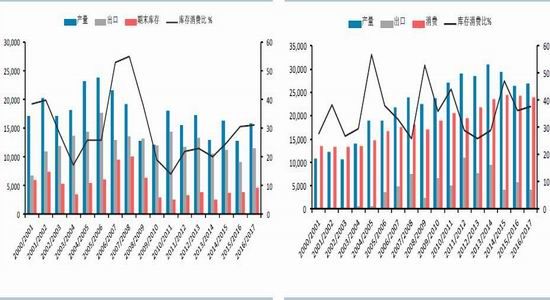

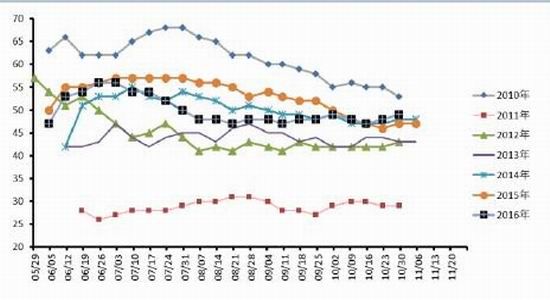

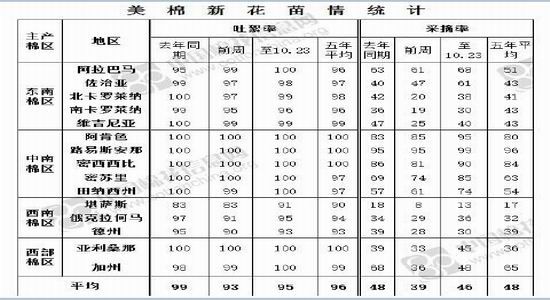

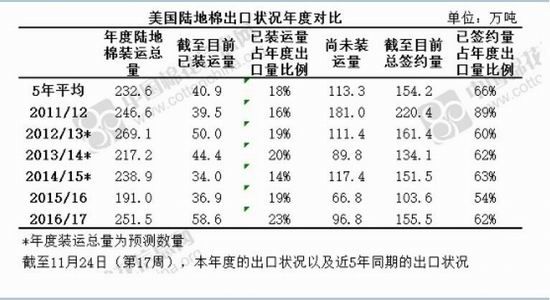

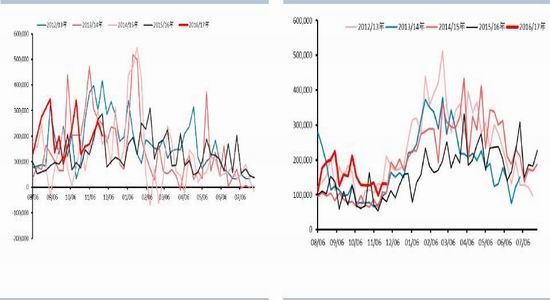

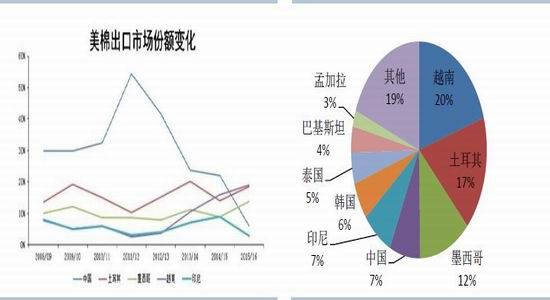

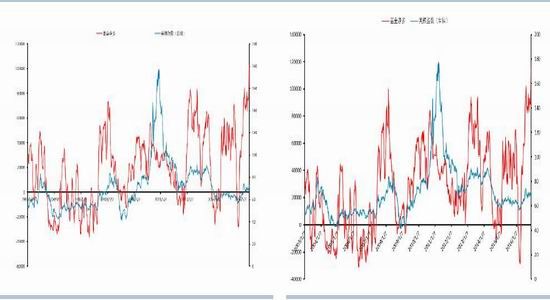

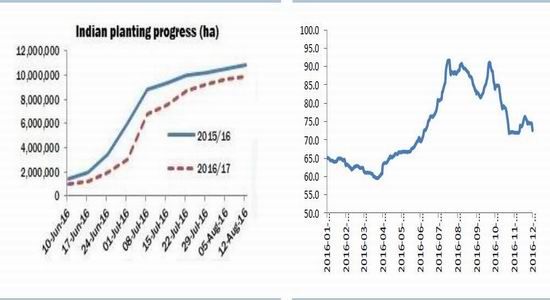

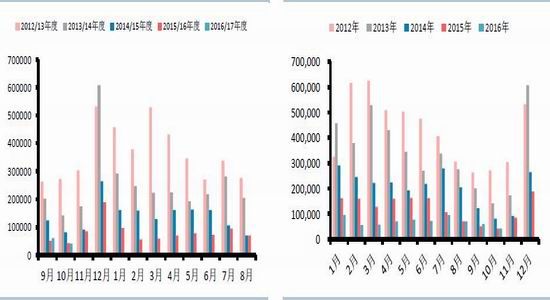

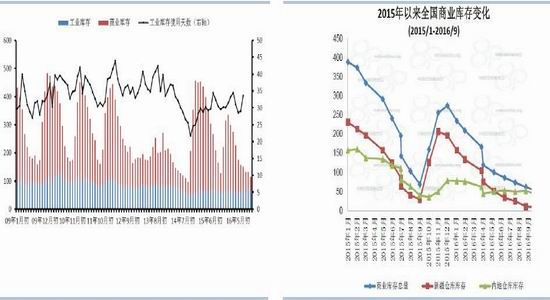

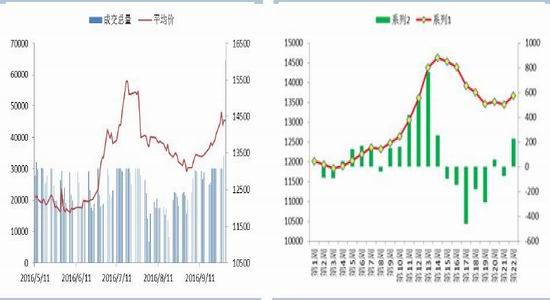

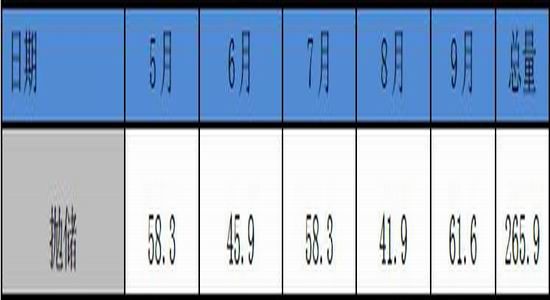

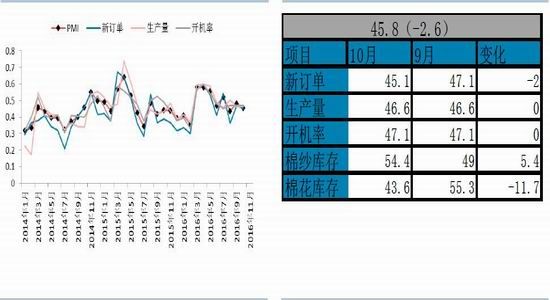

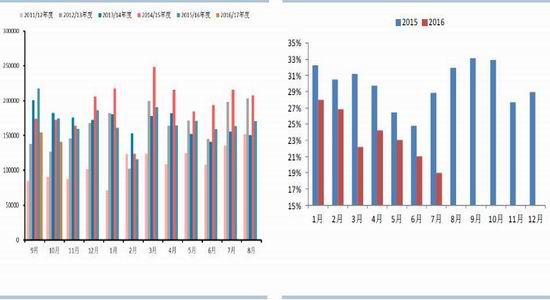

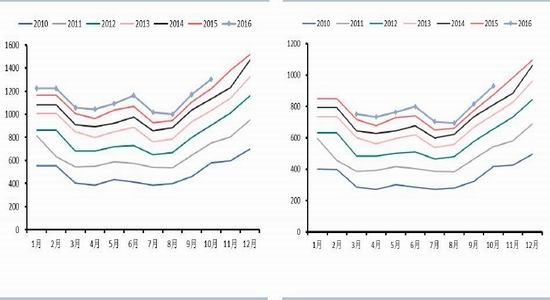

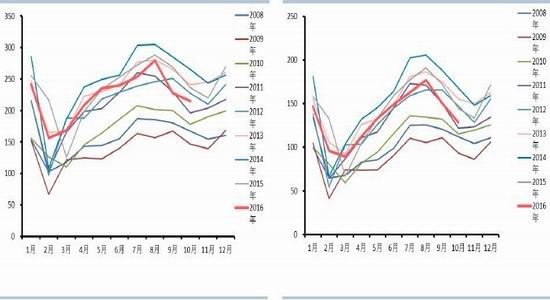

Client Summary Market Review: Looking back this month, with the rebound in Indian cotton prices and the overall export of US cotton, US cotton rose slightly. ICE March US cotton contract hit a maximum of 72.75 cents / lb, the lowest to 68.3 cents / lb, and finally closed at 71.54 cents / gang, an increase of 3.20%. On the domestic front, Zheng Cotton showed a strong volatility in the case of strong spot demand and increased demand for downstream textiles. In particular, the large fluctuations in cotton on November 11 brought a big impact on the market. As of the close of November 30, Zheng Cotton's 1701 contract rose 570 yuan / ton in January, an increase of 3.73%. US cotton market: According to the latest statistics from USDA, the harvest progress is 77% as of November 27, 77% in the same period last year, and 84% in 5 years. The overall harvest progress is slow. On the export side, the net contracted amount of upland cotton increased from last week. The latest data showed that the US net contracted exports for the week of 11.18-11.24 were 45,881 tons of upland cotton in 2016/17, and the shipment was 29,778 tons. The number decreased from last week and all exports were weak recently. Among them, China signed a net contract of 5,103 tons of US upland cotton in 2016/17. From the following statistical tables, as of November 24, the contracted volume accounted for 62% of the annual export, up from 54% in the same period of last year. The new year US cotton sales started well, and we will continue to pay attention to whether the export can continue to maintain strong. Cotton market in India: India's cotton price rebounded this month. The S-6 ginning factory picked up the price of 39,250 rupees/candela (about 73.05 cents/lb). At the end of November, it was affected by the Indian monetary policy and the cotton price rebounded. The latest foreign agricultural services report of the US Department of Agriculture shows that due to the increase in cotton production in northern India, the total cotton production in India will increase to 5.882 million tons this year, and the planting area will be adjusted to 157.5 million mu (10.5 million hectares). In addition, India's cotton exports this year are estimated at 850,000 tons. According to the report, due to the decrease in the total amount of Indian cotton purchased in the two traditional markets of Pakistan and China, the purchase volume in Bangladesh is also limited. The export volume of cotton in August and September in India fell to the lowest in 2012. According to Hindu Businessline, Pakistan’s “ambiguous ban†on Indian cotton will not have a major impact on its exports. Indian exporters said that Vietnam, Indonesia and other Asian markets and Brazil are very concerned about Indian cotton. In 2016/17, India's export shipments of cotton can still be between 93.5 and 1.02 million tons. Domestic cotton market: In November, new cotton continued to be listed in large quantities, and new cotton production is expected to be between 420-4.5 million tons. It is expected that by the time of dumping in March 17th, new cotton stocks will be less than 1 million tons. The tension in the cotton market is no less than the pre-storage period in May this year. The CCindex index (3128B) continued to strengthen this month, rising 641 yuan / ton in January. On November 24, the National Development and Reform Commission and the Ministry of Finance's State Reserve Cotton Storage Notice were officially released. In general, the market had expected this before. At present, it is only a short-term pressure on the futures market. On the spot side, the reaction is dull, and the downstream cotton yarn prices are gradually rising. Under the stimulus of the favorable factors, the market has limited impact. Summary: From an international perspective, the US agricultural report is bearish, the supply and demand layer is under pressure from cotton, and the pressure on the recent listing of new cotton in the northern hemisphere is still too large, but the Indian monetary policy has temporarily caused problems in the domestic cotton supply in India, making international cotton resistant to falling; Judging from the big pattern, the 16-year national reserve has gone smoothly, and the inventory has been relatively successful. The new-year inventory-to-sales ratio has dropped by 41% to 135%, and the fundamentals have further improved. The National Development and Reform Commission also announced the cotton storage policy, which caused a certain impact on the market. In November, cotton yarn prices rose and downstream demand increased. At the same time, the Corps increased the sales guidance price, but the cost support was obvious, and the commodity atmosphere was strong. Under the background of the depreciation of the Renminbi, Zheng Mian’s later shocks were stronger. Market review Looking back this month, with the rebound in Indian cotton prices and the overall good export of US cotton, US cotton rose slightly. ICE March US cotton contract hit a maximum of 72.75 cents / lb, the lowest to 68.3 cents / lb, and finally closed at 71.54 cents / gang, an increase of 3.20%. On the domestic front, Zheng Cotton showed a strong volatility in the case of strong spot demand and increased demand for downstream textiles. In particular, the large fluctuations in cotton on November 11 brought a big impact on the market. As of the close of November 30, Zheng Cotton's 1701 contract rose 570 yuan / ton in January, an increase of 3.73%. ICE main contract trend Zheng cotton main contract trend Source: Wenhua Finance, Huatai Futures Research Institute Global cotton market overview According to the forecast released by the US Department of Agriculture in November, the global cotton output in 16/17 was 22.486 million tons, an increase of 128,000 tons; consumption was 24.359 million tons, down 23,000 tons; ending stocks were 19.226 million tons, an increase of 208,000 tons The inventory consumption ratio increased by 0.88% compared with 78.85%. Overall, it is empty. In the US cotton market, the USDA increased its production in 16/17 by 28,000 tons to 3.519 million tons in the November supply and demand report. Consumption fell by 16,000 tons to 756,000 tons, and ending stocks increased by 44,000 tons to 980,000 tons. The inventory consumption ratio was 29.03%, an increase of 1.29 percentage points. Overall, the report is short. Domestically, the USDA for the 16/17 production is maintained at 4.572 million tons. We believe that this data has room for downward adjustment; consumption is maintained at 7.729 million tons; ending stocks are 10.472 million tons, which remain unchanged; inventory consumption ratio is 135.11%. stable. For domestic cotton, the report remains neutral. In India, the output of 16/17 is also increased by 109,000 tons to 5.879 million tons. We believe that there is still a possibility of downward adjustment in the later period; consumption will remain unchanged at 5.225 million tons, and exports will increase by 65,000 tons to 914,000 tons; The inventory was 2.513 million tons, an increase of 109,000 tons; the inventory consumption ratio was 40.94%, up by 1.36%, and the overall report was short. Global and major producing countries Source: USDA, Huatai Futures Research Institute Global Supply and Demand Balance Sheet China Supply and Demand Balance Sheet Source: USDA, Huatai Futures Research Institute US Supply and Demand Balance Sheet India Supply and Demand Balance Sheet Source: USDA, Huatai Futures Research Institute US cotton market analysis According to the latest statistics from the USDA, the harvesting progress was 77% as of November 27, 77% in the same period last year, and 84% in 5 years. The overall harvest progress was slow. US cotton excellent rate US cotton new flower seedling statistics Source: China Cotton Information Network, Huatai Futures Research Institute On the export side, the net contracted amount of upland cotton increased from last week. The latest data showed that the US net contracted exports for the week of 11.18-11.24 were 45,881 tons of upland cotton in 2016/17, and the shipment was 29,778 tons. The number decreased from last week and all exports were weak recently. Among them, China signed a net contract of 5,103 tons of US upland cotton in 2016/17. From the following statistical tables, as of November 24, the contracted volume accounted for 62% of the annual export, up from 54% in the same period of last year. The new year US cotton sales started well, and we will continue to pay attention to whether the export can continue to maintain strong. Annual comparison of US upland cotton exports Source: China Cotton Information Network, Huatai Futures Research Institute US cotton weekly contract (package) US cotton weekly shipments (package) Source: wind, Huatai Futures Research Institute US cotton export market share change over the years US cotton export share ratio this year Source: China Cotton Information Network, Huatai Futures Research Institute CFTC Futures Net Multiple Positions CFTC Futures + Options Net Multiple Positions Flower Information Network, China Source: wind, Huatai Futures Research Institute Indian cotton market analysis India's cotton price rebounded this month, S-6 ginning factory pick-up price of 39,250 rupees / kandi (about 73.05 cents / lb), the end of November was affected by the Indian monetary policy, cotton prices rebounded. The latest foreign agricultural services report of the US Department of Agriculture shows that due to the increase in cotton production in northern India, the total cotton production in India will increase to 5.882 million tons this year, and the planting area will be adjusted to 157.5 million mu (10.5 million hectares). In addition, India's cotton exports this year are estimated at 850,000 tons. According to the report, due to the decrease in the total amount of Indian cotton purchased in the two traditional markets of Pakistan and China, the purchase volume in Bangladesh is also limited. The export volume of cotton in August and September in India fell to the lowest in 2012. According to Hindu Businessline, Pakistan’s “ambiguous ban†on Indian cotton will not have a major impact on its exports. Indian exporters said that Vietnam, Indonesia and other Asian markets and Brazil are very concerned about Indian cotton. In 2016/17, India's export shipments of cotton can still be between 93.5 and 1.02 million tons. Indian cotton planting progress Indian cotton domestic price trend (cents per pound) Source: China Cotton Information Network, Huatai Futures Research Institute Domestic cotton market analysis Supply side: production + import + inventory + throwing storage According to the latest survey of China Cotton Information Network, the national cotton planting area in 2016 is expected to be 40.28 million mu, a decrease of 10%. In terms of regions, the area of ​​cotton planting in Xinjiang was 30,600 mu, a decrease of 6%; the area of ​​cotton planting in the interior was 10.22 million mu, a decrease of 22%. Domestic cotton production in 16/17 is expected to be around 4.47 million tons, including a total output of 3.67 million tons in Xinjiang and 800,000 tons in the mainland. In November, new cotton continued to be listed in large quantities, and new cotton production is expected to be between 420-4.5 million tons. It is expected that by the time of dumping in March 17th, new cotton stocks will be less than 1 million tons, and the domestic cotton market will be tight. It is no less than the pre-storage period in May this year. The CCindex index (3128B) continued to strengthen this month, rising 641 yuan / ton in January. On November 24, the National Development and Reform Commission and the Ministry of Finance's State Reserve Cotton Storage Notice were officially released. In general, the market had expected this before. At present, it is only a short-term pressure on the futures market. On the spot side, the reaction is dull, and the downstream cotton yarn prices are gradually rising. Under the stimulus of the favorable factors, the market has limited impact. Domestic cotton planting area in 2016 Source: China Cotton Information Network, Huatai Futures Research Institute In terms of imports, cotton imports have been shrinking this year, and the latest October data is relatively low. In October 2016, China imported 41,300 tons of cotton, a decrease of 31.62% from the previous month and a decrease of 1.67% from the same period last year. In the first ten months of 2016, the cumulative import was 698,200 tons, a year-on-year decrease of 41.82%. Domestic cotton stocks are high, and the destocking road is long and winding. Under such a background, it is expected that in 2016/17, the policy on imported cotton will not be relaxed, and the 1% tariff quota of 894,000 tons is still the main. Will exceed 1 million tons. Cotton imports (crop year) cotton imports (natural year) Source: China Cotton Information Network, Huatai Futures Research Institute In terms of inventory, domestic industrial and commercial inventories have declined rapidly since the beginning of the 16th year. Due to the lack of confidence in the market at the beginning of the year, both commercial and industrial inventories remained low. In September, the new cotton market was postponed, and the reserve cotton continued to dominate the market. Textile enterprises were highly motivated to purchase reserve cotton, and social commercial stocks continued to decline. The latest data shows that commercial inventories at the end of September were 507,000 tons, a decrease of 104,000 tons from the previous month, a drop of 17%. Among them, Xinjiang's Xinjiang cotton is 84,500 tons, the mainland warehouse is 365,500 tons, and the bonded area is 57,000 tons. As of the end of September, the industrial inventory was 464,600 tons, a decrease of 66,800 tons. The average daily inventory of cotton was about 33.6 days, an increase of 4.5 days from the previous month and a decrease of 0.9 days from the same period last year. China's cotton industrial and commercial stocks Source: China Cotton Information Network, Huatai Futures Research Institute In August, under the influence of the bad news of the postponement of the reserve, the reserve price of the reserve cotton fell, and the market sentiment was bleak. In July, the basic daily turnover rate was 100%, and in August, it was only about 60%. The enthusiasm of downstream textile enterprises to receive goods plummeted. Back in September, textile companies received a enthusiasm for receiving goods, and by the end of September, the volume was close to 100%. In the end, all the reserves reached 2.659 million tons. According to the announcement of the National Development and Reform Commission and the Ministry of Finance on November 24, this year's new cotton listing period (currently until the end of February next year) The reserve cotton rotation will not be arranged. The 2017 reserve cotton round sales will start from March 6th. The deadline is tentatively set at the end of August, and the daily listed sales volume will be arranged at 30,000 tons. For example, if the domestic and international market prices increase rapidly and the reserve price of reserve cotton sales exceeds 70% in the past three days, the number of listings will be increased and the sales time will be extended. 2016 reserve cotton round-off transaction 2016 reserve cotton round-off price per week Source: China Cotton Information Network, Huatai Futures Research Institute Estimation of the total amount of reserve cotton in 2016 Source: Huatai Futures Research Institute Downstream consumption: yarn → cotton → textile clothing The downstream cotton spinning industry has improved. In October 2016, the China Cotton Textile Industry Purchasing Managers Index (PMI) was 45.8%, down 2.6 percentage points from the previous month. In October, domestic cotton in Xinjiang was gradually listed in large quantities. The textile mills consumed stocks of reserve cotton. The new cotton was accompanied by the market and a small amount of purchases. It is worth "Silver 10". Although the new orders are reduced, they are still acceptable. Some companies expect orders to decrease after November. Cotton textile industry PMI cotton spinning PMI change in the month Source: China Cotton Information Network, Huatai Futures Research Institute The price of downstream yarns rebounded this month. The domestic price index of 32 carded yarns was up to 22,880 yuan/ton, up by 340 yuan/ton; the price index of 40 combed yarns was 26,040 yuan/ton, up 280 yuan/ton. In terms of profit, due to the increase in the spot price of cotton yarn this month, the profit has dropped. We calculate the profit margin at the current yarn price, and the price of raw cotton is 16076 yuan/ton. In terms of imported cotton yarn, the import of cotton yarn declined in 2016, in line with our forecast at the beginning of the year. In October, China's cotton yarn import month was 140,700 tons, a year-on-year decrease of 19.24% and a decrease of 8.59% from the previous month. From January to September 2016, the cumulative import of cotton yarn was 1,591,700 tons, a year-on-year decrease of 20.39%. The decline in the volume of imported cotton yarn is mainly from India. Indian yarn has always occupied the leading position in the domestic imported yarn market. However, India’s domestic cotton price has been reduced in 15/16, and domestic cotton prices have soared, which in turn has led to an increase in Indian yarn prices. The advantages gradually faded. The decline in the market share of the Indian yarn is a big plus for domestic yarns, and the domestic yarn market share will increase. However, the price of outer yarn has fallen recently, and the import volume is expected to pick up later. In terms of pure cotton fabrics, there were not many bright spots this year and the prices were relatively stable. Orders are relatively average, the overall operating rate is 60-65%, long-term orders are relatively lacking, and profits are also average. KC32S price trend and profit JC40S price trend and profit Source: China Cotton Information Network, Huatai Futures Research Institute China's cotton yarn imports Source: China Cotton Information Network, Huatai Futures Research Institute Yarn inventory (days) stock of cloth (days) Source: China Cotton Information Network, Huatai Futures Research Institute The textile and garment industry as a whole showed a slight recovery, with domestic sales increasing year on year, but exports continued to decline. According to the latest data from the General Administration of Customs, in October 2016, China’s textile and apparel exports were approximately US$21.46 billion, a decrease of 9.28% year-on-year. Among them, export yarns, fabrics and products were US$8.598 billion, down 6.64% year-on-year; apparel and clothing accessories were US$12.862 billion, down 10.96% year-on-year. From January to October 2016, China's cumulative export of textile and apparel was approximately 222.561 billion US dollars, a year-on-year decrease of 5.31%. Among them, the export of clothing was 134.429 billion US dollars, a year-on-year decrease of 6.62%. Retail sales of textiles and clothing (100 million yuan) Retail sales of clothing (100 million yuan) Source: wind, Huatai Futures Research Institute Textile and apparel exports (100 million US dollars) Clothing exports (100 million US dollars) Source: China Cotton Information Network, Huatai Futures Research Institute In terms of alternatives, the latest data shows that the latest polyester price of polyester is about 7,510 yuan / ton, which is stable and rising. It is expected to form a support for cotton prices; viscose staple fiber is 15,240 yuan / ton, and the price of glue is falling, then the price is formed. pressure. Cotton and polyester price difference Source: China Cotton Information Network, Huatai Futures Research Institute to sum up From an international perspective, the US-Agriculture report is bearish, the supply and demand layer is under pressure from cotton, and the pressure on the recent listing of new cotton in the northern hemisphere is still too large, but the Indian monetary policy has temporarily caused problems in the domestic cotton supply in India, making international cotton resistant to decline; In the big picture, the 16-year national reserve has gone smoothly, and the inventory has been relatively successful. The new-year inventory-to-sales ratio has dropped by 41% to 135%, and the fundamentals have further improved. The National Development and Reform Commission also announced the cotton storage policy, which caused a certain impact on the market. In November, cotton yarn prices rose and downstream demand increased. At the same time, the Corps increased the sales guidance price, but the cost support was obvious, and the commodity atmosphere was strong. Under the background of the depreciation of the Renminbi, Zheng Mian’s later shocks were stronger. Huatai Futures Xu Sheng experience half zippers Unisex sportswear Guangzhou LIDONG Garment Industrial Co., Ltd. , https://www.lidongsports.com